Can Ethereum Redefine Sustainable Crypto Corporate Treasuries Beyond Bitcoin?

Introduction

In August 2020, MicroStrategy (now branded as Strategy) shocked the financial world by allocating millions of its corporate treasury to Bitcoin, pioneering a strategy once considered unthinkable but now widely adopted by public firms to hedge inflation and unlock value. As Bitcoin solidifies its place in corporate finance, a new question emerges: could altcoins like Ether offer firms even greater opportunities for growth, innovation or diversification? This article explores why some firms are venturing beyond Bitcoin to adopt Ether as treasury asset, investigating whether this bold strategy can replicate MicroStrategy’s success. By examining the potential for higher returns, exposure to innovative blockchain ecosystems, and the long-term sustainability of this approach, I aim to uncover whether Ether represents a sustainable treasury option for corporate firms in 2025 and beyond.

Article Objective

This article seeks to determine whether publicly listed firms can successfully adopt Strategy’s leveraged Bitcoin treasury strategy for Ether, with the tenet revolving around this term called mNAV (market Net Asset Value):

mNAV = Market Capitalisation of Firm / Current value of token holdings

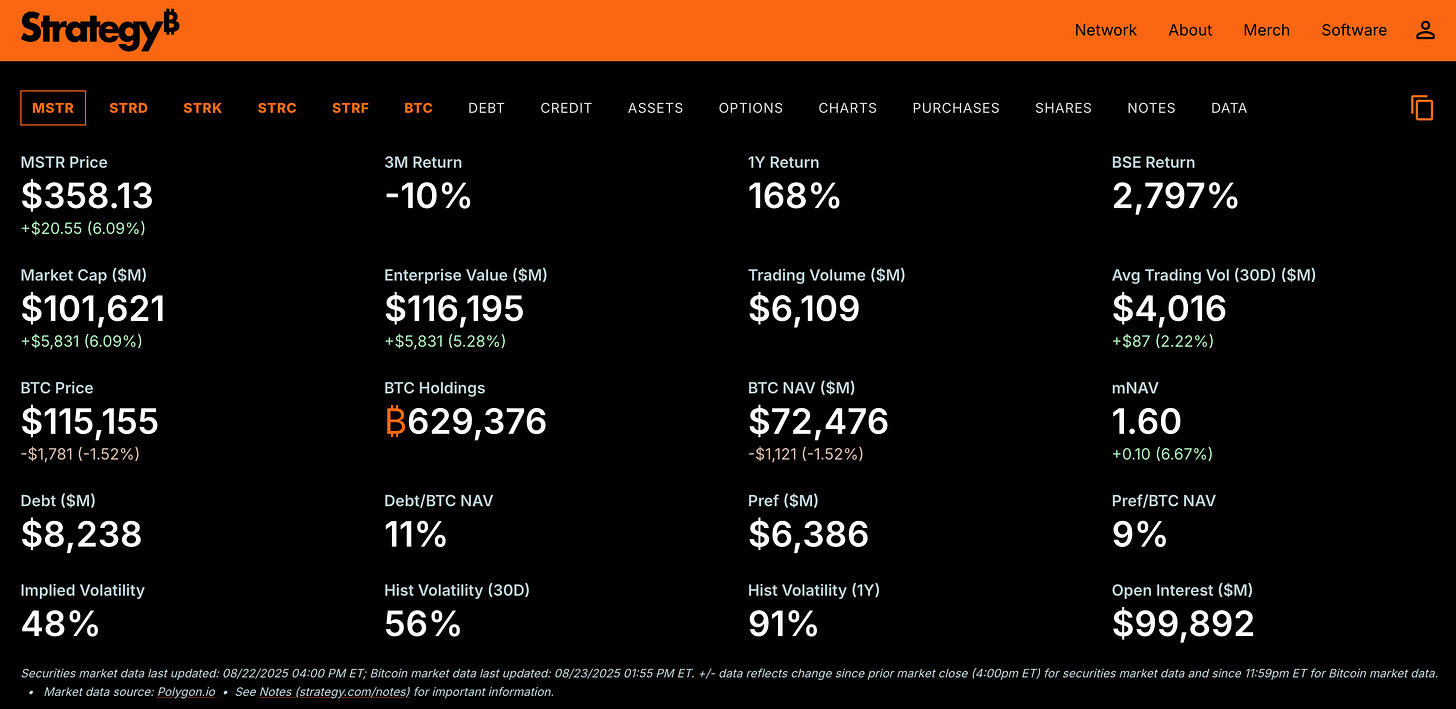

This metric is crucial, as it helps readers understand why these treasury-holding firms are obsessed with it. It explores why some firms are choosing Ether over Bitcoin, despite Strategy’s proven success with its 629k BTC holdings (worth $72.5 bn in Aug 2025) and an mNAV at 1.6. Potential advantages of Ether include higher returns due to their growth potential, diversification beyond Bitcoin’s “store-of-value” role and participation in innovative blockchain ecosystems, such as Ether’s staking (locking ETH to support the network for yields) and decentralised finance (DeFi) applications. Hence, this article aims to uncover whether Ether treasury strategies can deliver superior risk-adjusted returns or “alpha” while navigating higher uncertainty. To evaluate this, we first examine how Strategy’s leveraged financing model drives its mNAV premium, providing a blueprint for firms considering Ether.

Funding Strategy

Strategy’s Bitcoin treasury strategy, launched in 2020, was driven by the need to protect corporate value against inflation and capitalise on Bitcoin’s potential as a store of value. Per BCB group article, Michael Saylor mentioned Bitcoin was ultimately chosen due (1) “cost of capital” (the return needed to outpace inflation and opportunity costs) which spiked to 25% due to stimulus-driven asset inflation and low yields on traditional assets like bonds, resulting in these assets not being able to hold up its store of value and (2) IRS’s (US’s tax authority) guidance which indicates that Bitcoin should be treated as a property rather than currencies which results in the asset being treated less sophisticated from a tax perspective relative to holding currencies.

As Bitcoin’s price rose, Michael Saylor capitalised on significant gains by raising funds from investors. The capital raise can be simply divided into 2 parts: (1) Equity and (2) Debt;

(1) Equity:

- At-the-Market (ATM) Stock Sale: Strategy sells MSTR Class A common stock directly into the capital market. Simple and direct.

- Preferred Stocks: The buyers of the convertible notes will receive a fixed dividend at “X” % amount but they do not have the ability to vote like how common shares do. Example of these preferred stocks include STRF or STRD which offers 10% dividend on par value of $100.

(2) Debt:

- Convertible notes: These are debt instruments with a fixed maturity date but include an option for noteholders to convert the notes into MicroStrategy’s Class A common stock at a predetermined conversion price. For example, Strategy’s $3 bn 0% Convertible Senior Notes due 2029 allows investors to convert their convertible notes to common shares at a strike of $672.40 per share for the 2029 notes, representing a 55% premium over the stock price at issuance, thus delaying shareholding dilution.

Source: Strategy (https://www.strategy.com/)

By raising capital through equity and debt, Strategy grew its Bitcoin reserves to almost 630k BTC, worth approximately ~$72.5 bn as of Aug 2025, while sustaining a market valuation premium reflected in its 1.6 mNAV.

Importantly, Strategy issues new shares as mNAV is traded at a premium (mNAV> 1), it sells them for more than the current NAV per share. For example, with an mNAV of 1.6 and a hypothetical NAV per share of $100, new shares are sold for $160. The additional $60 raised adds to the firm’s cash, funding more Bitcoin purchases that increase total NAV (assets minus liabilities). Since the number of shares doesn’t grow proportionally, NAV per share rises, reinforcing investor confidence and the positive flywheel effect.

This leveraged financing strategy enables Strategy to acquire significantly more Bitcoin than its cash reserves would permit, driving an mNAV range of 1.6–2.1 in 2025, where its enterprise value (market capitalisation + debt + preferred stock - cash holdings) exceeds the $72.5 bn market value of its 630k Bitcoin holdings. With an enterprise value of approximately $116 bn in Aug 2025, Strategy’s mNAV of ~1.6 reflects investor confidence in its ability to increase Bitcoin per share through low-cost capital raises, such as 0% convertible notes and ATM sales.

This approach is more cost-effective than traditional bank loans, which often carry higher interest rates and protects Strategy’s Bitcoin treasury during steep price declines by structuring the debt as non-recourse, limiting creditor claims to the terms of the notes rather than the company’s Bitcoin or other assets. For investors, this leverage amplifies returns. For example, a 10% Bitcoin price increase could boost Strategy’s stock by more than 10% due to the mNAV premium but introducing risks of amplified losses if Bitcoin’s price falls.

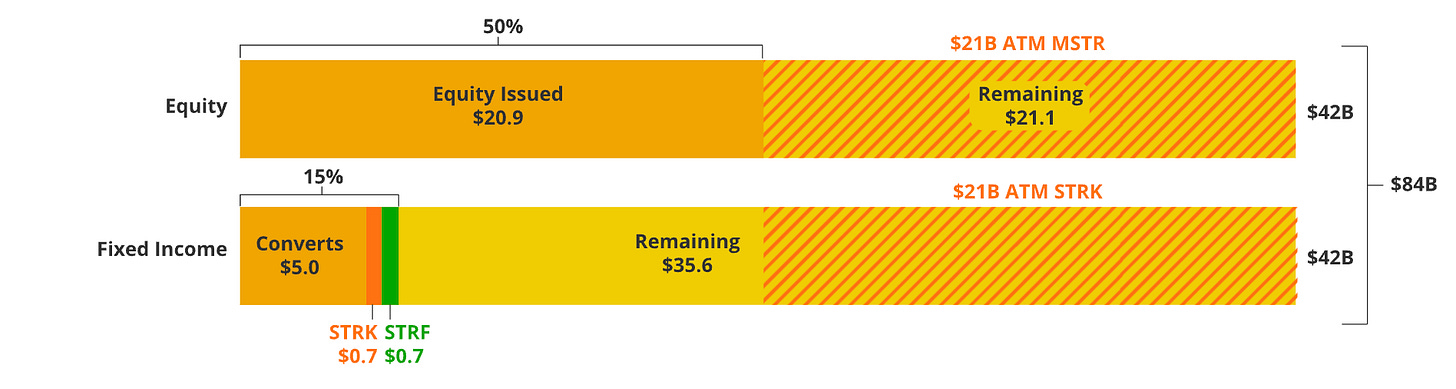

Source: VanEck - diagram shows the breakdown of the proposed $84 bn planned to be raised by MicroStrategy

Strategy’s financing model, as outlined in VanEck’s breakdown of its proposed $84 bn capital raise, demonstrates how leverage sustains a high mNAV, offering a blueprint for altcoin treasury strategies. The next section explores why publicly listed firms are choosing Ether and whether their leveraged approaches could work, balancing higher return potential against increased risks. This shift to Ether hinges on execution, detailed next.

Why Ether?

Having established how Strategy’s leveraged financing model sustains its Bitcoin treasury, the next question is whether this approach can be adapted for altcoins like Ethereum.

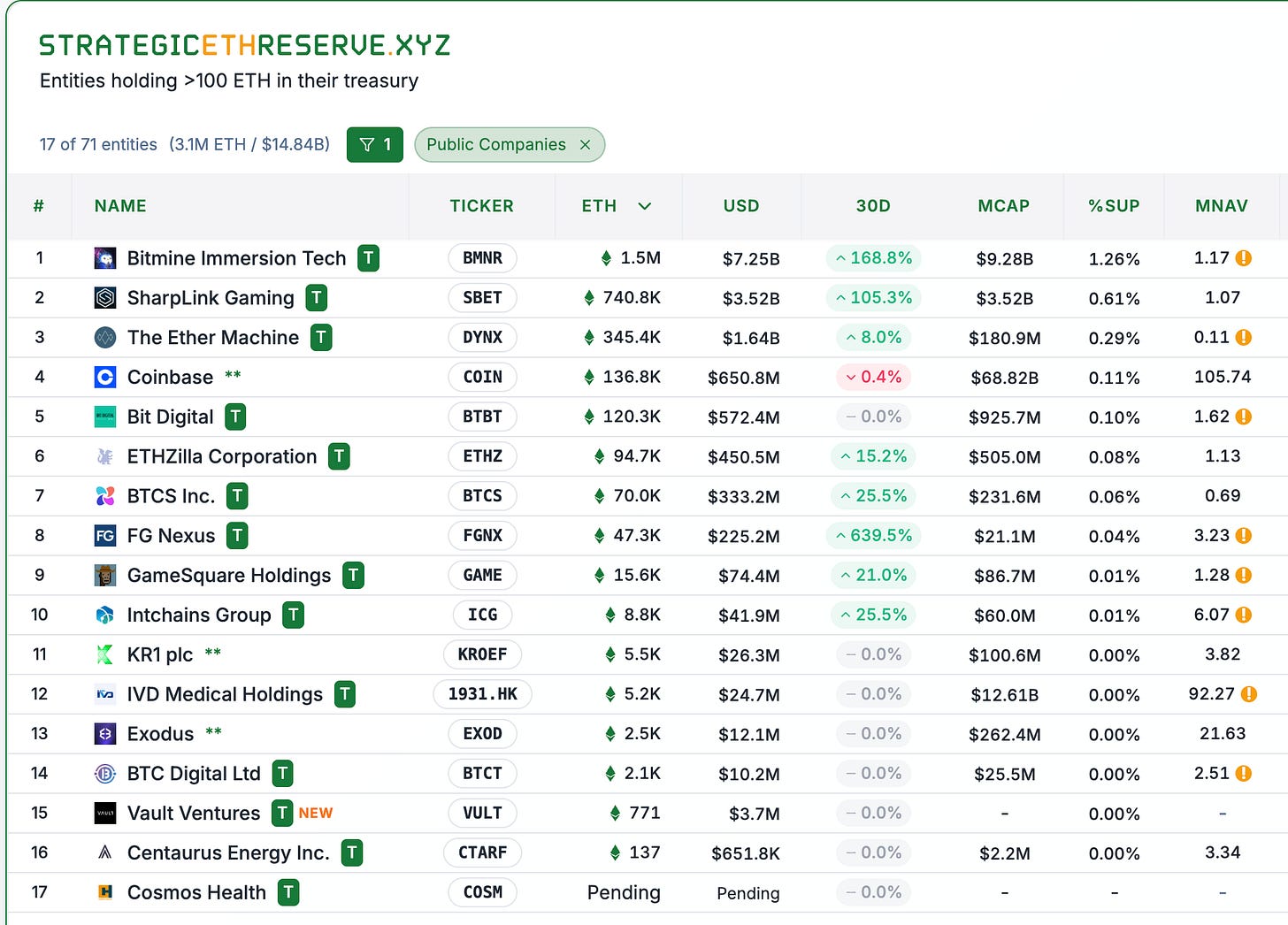

Source : StrategicETHReserve.xyz

Source : StrategicETHReserve.xyz and GameSquareHoldings (mNAV amended to 0.84 per website).

The list above shows 8 publicly listed firms (excluding centralised exchanges like Coinbase). These firms have either crypto as their main source of operation such as BTCS Inc, which is involved in Bitcoin mining or could have exposure to crypto due to management. For example, SBET’s hiring of Joseph Chalom as co-CEO who is known to spearhead Blackrocks’s digital assets initative.

From my readings, the general theme for these firm to explore holding Ether stem from these reasons:

- Growth Potential - Ether has a relatively smaller market cap compared to BTC, potentially offering higher returns due to their growth trajectories. This would provide shareholders with superior risk-adjusted returns relative to BTC. For instance, the CAGR for Ether currently stands at ~62.8% p.a from the past 5 years (year 2020). However, it is worth noting that historical returns are not representative of future returns.

- Staking yields - As Ether offers staking yields, the general idea is that there is a premium that could be generated from staking their holdings. Let’s do a rough estimation calculation and simplify the calculations. Say a firm is planning to hold Ether into perpetuity with a value of $100, with the discounted rate of 20% (assume investor’s desired rate for crypto return is 20% p.a). Assume a 5% staking yield, the firm could expect a premium of 25% on their mNAV solely from staking itself.

- Innovation - Firms holding these altcoins are actively engaging and supporting the development of the ecosystem such as Ether staking, DeFi or scalable dApps which offers more value than the role played by BTC’s “store-of-value“ role.

- First and early-mover advantage - Firms adopting altcoins could position themselves as pioneers in ETH treasury holdings, mirroring Strategy’s 2020 breakthrough and attract investor interest as institutional adoption of ETH gains momentum. This in turn provides a very good risk-to-reward ratio as buying demand is speculated to pickup when more institutional investors could participate. To add, I believe to a certain extent firms are even trying to front-run the process to be the firm holding the largest amount of Ether. This signals to the masses that they are the “preferred” companies when it comes to capital raising and execution of Ether purchase. This action also signals credibility and attract capital due to its scale and efficiency in acquiring Ether.

Success Factors

On the surface, one might assume these treasury companies succeed due to their sophisticated and often opaque models promising exponential growth, claiming “XYZ” token could 100x in “N” years, yet I believe these advantages hinge on execution, particularly the momentum of accumulation and efficient capital raising, which are critical to sustaining altcoin treasuries.

(1) Momentum of accumulation

Their ability to raise capital and how aggressive they are at executing the strategy of buying up Ether.

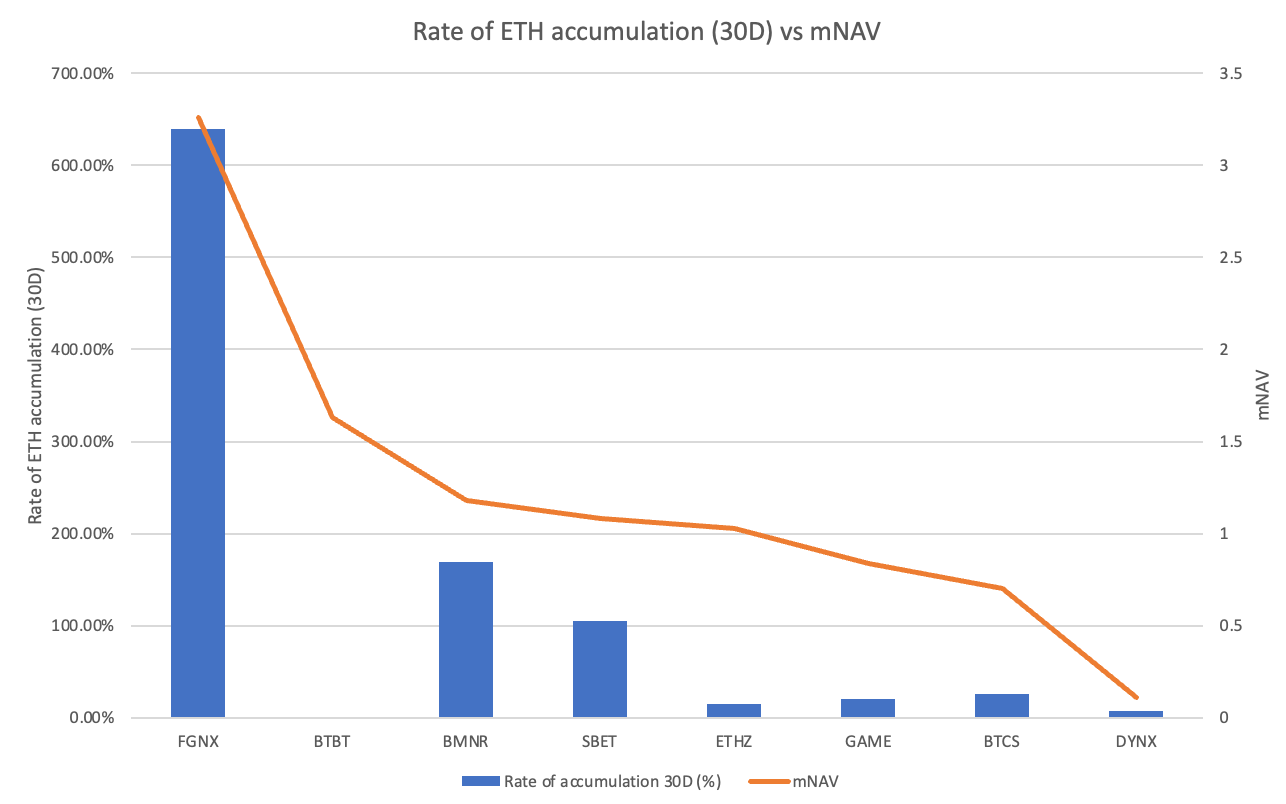

Rate of Ether accumulation vs mNAV

What stood out is that FGNX stands out massively with a 639% accumulation rate in 30 days. That’s enormous relative to other tickers is due to the fact on how FGNX recently acquired $200m worth of Ether and has plans to acquire up to 10% of the current Ether supply, announced in July 2025. BMNR and SBET are also notable, with 169% and 105% accumulation respectively and they’re still actively adding to their reserves. Others (GAME, BTCS, DYNX) are showing only modest growth (under 30%), with BTBT at 0%, meaning no new Ether accumulation recently. It is evident that the firms with the highest accumulation rate (FGNX, BMNR, SBET) are the ones maintaining higher mNAV multiples (>1) with the exception of BTBT. I believe the reason could be due to how BTBT is winding down their mining operations due to lower yield and pivoting their strategy to Ether treasury holdings, potentially well received by the market.

To discuss, the high-accumulators continue to command higher mNAV premiums. For example, BMNR has solidified its lead as the world’s largest Ether treasury holder, with 1.52 million Ether, driven primarily by aggressive ATM (at-the market) equity raises with an even grander ambition to raise up to $20 bn to purchase more. This strategy is followed closely by SBET, which maintained their steady accruals via similar mechanisms. Slower firms like DYNX (post-SPAC merger with ~345K ETH) and BTCS (~70K ETH) have seen minimal net additions, with BTCS focusing on dividend payouts in Ether, rather than pure stacking.

This could suggest that firms that are actively and continously building their reserves like FGNX, BMNR, SBET, are seen as credible Ether treasury players and have their mNAV > 1 while firms with slower accumulation struggle to command premiums (mNAV < 1). This suggests investors are valuing not just the size of the Ether on balance sheet, but the momentum of accumulation.

This pattern indicates a self-reinforcing mechanism where, in order for these firms to survive, they need to be good at raising capital (e.g., by issuing shares) at a premium value. This results in an increased in net asset value per share, attracting further investments and ultimately boosting its treasury growth sustainably. Conversely, low momentum triggers a ‘spiral of doom.’ When mNAV nears or falls below 1, capital raises become harder as raising money grows more challenging. Selling more shares at a lower price reduces the value per share, creating a downward spiral that can hurt the firm. This could lead to stagnation and further discounts from short sellers or outflows. Hence, this explains why firms like DYNX and BTCS, where post-merger challenges or ETH based dividend payouts signal reduced aggression, struggle with mNAV premiums.

Whereas in BTC treasuries, with more than 79+ public firms holding more than 4.5% of the supply which pioneered the trend but are slowing down. Also, about 1/3 of these firms trade below their net asset value, premiums are shrinking. For example, MSTR’s mNAV used to trade at 4x to current ~1.61x despite BTC hitting all time highs. It is also worth noting that the dominance of one leader in BTC (MSTR’s BTC stash is 12x more than their nearest competitor i.e MARA holdings) also limits growth for others, unlike Ether’s relatively pioneer stage where BMNR is only 2x of SBET in terms of the Ether stash.

(2) Capital raising strategy

The secondary aspect in my opinion comes down to how efficient these operators could raise capital from investors. It is by no means an easy feat considering how BMNR is attempting to raise up to $24.5 billion ($4.5 billion raised + $20 billion goal target), which comes at an expense of existing shareholders as this exercise would dilute the existing shareholders. However, efficient capital raising when done at mNAV premiums (>1x) turns this financial alchemy into a net positive by increasing net asset value (NAV) per share. This is achieved when BMNR issues shares at an mNAV premium (e.g., 1.18), selling them above NAV (e.g., $118 for a $100 NAV share). The extra $18 per share boosts cash for Ether purchases, increasing total NAV (assets minus liabilities) and with limited dilution, raising NAV per share.

A prime example is BMNR’s ATM stock sale programme which began with $250mm on July 9th increasing to $2 bn by July 24th. As recent as Aug 12th, this target commitment went up to $24.5 bn in total. BMNR’s target purchase of 5% ETH supply signifies a bolder bet than Strategy’s where $84 bn is used to target a lesser portion of BTC supply. BMNR’s $24.5bn commitment for 5% of ETH supply (6m Ether) is more aggressive proportionally. By leveraging its 10.8 bn firm market cap, BMNR seeks outsized treasury growth. This could drive higher mNAV premiums from current mNAV premium of 1.2, triggering a positive flywheel effect where increased investor confidence enables more capital raises, further boosting ETH holdings and NAV per share.

On the flip side, if the mNAV drops below 1 (e.g. DYNX at 0.11), they are essentially issuing shares at a discount ($11 for a $100 NAV share) raises only $11M per million shares, adding little Ether to the treasury while diluting NAV per share to ~$90. This situation erodes value, triggering a “spiral of doom” with further discounts which isn’t good for shareholders. Hence, you wont be surprised to see if firms will try to employ strategies to buyback their shares instead of Ether if their mNAV approaches 1 or below 1.

Conclusion

To conclude, while Strategy’s Bitcoin treasury model has set a precedent with sustained mNAV of above 1, Ethereum offers a compelling alternative for firms seeking higher growth, yield and system innovation. Firms like BMNR, SBET, FGNX demonstrate that through aggressive accumulation and efficient capital raising at mNAV premiums (>1x) can drive sustainable treasury-holding model, mirroring Strategy’s success. However, given the increasing competition and number of firms adopting this strategy, firms that fail to meet the cut will struggle, as seen in DYNX and BTCS unless a new catalyst emerges. As institutional adoption grows, evidenced by over 3M ETH held by treasuries in 2025. Ether could emerge as the sustainable alternative, potentially delivering superior risk-adjusted returns if firms navigate the ‘spiral of doom’ pitfalls. Ultimately, the future of Ether treasuries hinges on execution with 2025 poised to test whether this strategy can outpace Bitcoin’s proven, yet maturing path.

As usual, thank you to my friends for their proofreading and insightful feedback. I’d love to hear your thoughts in the comments and explore mNAV analysis for other tokens if anyone is keen!

Disclaimer:

- This article is reprinted from [Terry’s Takes]. All copyrights belong to the original author [@terryleetr">Terry Lee]. If there are objections to this reprint, please contact the Gate Learn team, and they will handle it promptly.

- Liability Disclaimer: The views and opinions expressed in this article are solely those of the author and do not constitute any investment advice.

- Translations of the article into other languages are done by the Gate Learn team. Unless mentioned, copying, distributing, or plagiarizing the translated articles is prohibited.

Related Articles

Solana Need L2s And Appchains?

The Future of Cross-Chain Bridges: Full-Chain Interoperability Becomes Inevitable, Liquidity Bridges Will Decline

Sui: How are users leveraging its speed, security, & scalability?

Navigating the Zero Knowledge Landscape

What is Tronscan and How Can You Use it in 2025?